Portability

A provision of the Save Our Homes (SOH) Amendment to the Florida Constitution allows homestead property owners to port, or transfer, the accumulated difference between assessed value and the just/market value. The process of moving this SOH differential (or benefit) from one property to another is referred to as Portability. Portability must be applied for and applications must be submitted by March 1st of the year being applied for. Apply quickly and easily using the "Apply Online" button above and read on for more information and scenarios. You can also click here to be redirected to the Florida Dept. of Revenue for additional information and the paper application.

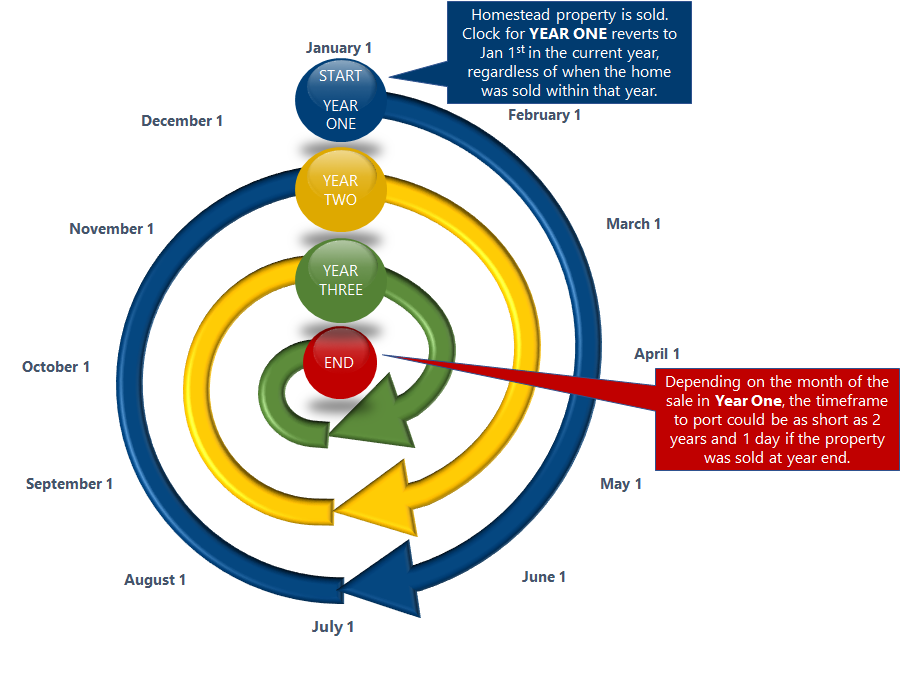

During the November 3rd, 2020 election, voters approved to expand the portability window to three tax years. The information below is designed to provide better understanding of this change to Florida law (effective date of January 1, 2021).

- Time limit to port the SOH benefit to a new homestead property is 3 tax years from January 1st of the last qualified homestead exemption, not 3 years from the date of sale (see time spiral graphic below). Please note that a sale late in a year could reduce the qualifying time window down to as little as 2 years in a worst-case scenario (sale closing on last day of the year). The intent of this legislation was to always provide a transfer window of at least a minimum of 2 years to align with voter perception from when portability originally passed in 2008.

Sample Scenario

If you sell your homestead property in any month in 2024, the last qualified homestead exemption date is considered to be January 1, 2024. This is the date from which the 3-year transfer window is calculated. Therefore, you would have until January 1, 2027 to qualify for a new homestead exemption and port the SOH benefit to your new Florida homestead property.

FAQs about Portability

What is the maximum amount that can be ported (transferred)?

$500,000 of value (difference between Just/Market Value and Assessed Value).

How is the portability amount impacted by an upsizing or downsizing in Just/Market Value?

Upsizing - if the just/market value of the new homestead is greater than or equal to the previous home's just/market value, the entire SOH benefit value can be transferred up to the $500,000 limit.

Downsizing - if the just/market value of the new homestead is less than the previous home's just/market value, a percentage of the accumulated SOH benefit can be transferred, subject to the $500,000 limit. For example, moving from a property with a Just/Market Value of $300,000 down to one at $180,000 would result in 60% of the SOH benefit amount being eligible for transfer to the new homestead ($180,000 / $300,000 = 60%).

When is the deadline to apply for Portability?

Must be submitted by March 1st of the year being applied for.

Does the Tax Estimator on your website take into account portability?

Yes. To help you calculate what property taxes may be, our office created a Tax Estimator. This tool allows buyers (and their lenders) to more accurately estimate property taxes under new ownership. The tax estimator works for both first time buyers and relocating buyers as it considers any benefit they may receive from transferring their SOH benefit.

An Example of Portability

| Former Homestead | |

|---|---|

| Just/market value is $300,000 | As of January 1, in the year of sale. |

| Assessed value is $200,000 | As of January 1, in the year of sale. |

| Taxable value is $200,000 - $50,000 = $150,000 | Assessed value less homestead exemption. |

|

Save Our Homes (SOH) benefit is |

Just/market value less assessed value. |

|

UPSIZING to a home with a Just/Market Value of $400,000 |

A move to a higher valued home entitles you to port the full $100,000 benefit (maximum allowable $500,000) from your former homestead. |

|---|---|

| Just/market value of new home is $400,000 | As of January 1, in the year after purchase. |

| Portability benefit is $100,000 | Full portability benefit of former home. |

| New Assessed Value is $400,000 - $100,000 = $300,000 | Just/market value of new home less portability benefit. |

| Taxable value is $300,000 - $50,000 = $250,000 | New assessed value less homestead exemption. |

| Save Our Homes (SOH) benefit is $300,000 - $200,000 = $100,000 |

Just/market value of new home less the new assessed value. |

|

DOWNSIZING to a home with a Just Value of $200,000 |

A move to a lower valued home entitles you to port a percentage of the $100,000 benefit (maximum allowable $500,000) from your former homestead. |

|---|---|

| Just/market value of new home is $200,000 | As of January 1, in the year after purchase. |

| Pro-rated portability benefit is ($200,000/$300,000) x $100,000) = $66,667 |

Just/market value of new home, divided by the just/market value of the former home, then multiplied by the portability benefit from the former home. |

| New assessed value is $200,000 - $66,667 = $133,333 | Just/market value of new home less the pro-rated portability benefit. |

| Taxable value is $133,333 - $50,000 = $83,333 | New assessed value less homestead exemption. |

| Save Our Homes (SOH) benefit is $200,000 - $133,333 = $66,667 |

Just/market value of new home less the new assessed value |